Sammy Gyamfi, better known as the fiery communicator of Ghana’s opposition in years past, now finds himself at the helm of a sensitive economic initiative – and under intense scrutiny. As the Chief Executive Officer of the Ghana Gold Board (popularly called GoldBod), Gyamfi is tasked with defending a flagship program that trades Ghana’s gold for foreign exchange reserves. The International Monetary Fund (IMF) recently revealed that this “Gold-for-Reserves” scheme incurred an eye-popping loss of about $214 million by the third quarter of 2025. In response, Gyamfi has mounted a vigorous public defense of GoldBod’s operations and the government’s handling of the program. His commentary, however, has raised questions about the credibility of his arguments, the transparency of GoldBod’s dealings, and the political ramifications for the ruling party.

GoldBod and the $214 Million Controversy

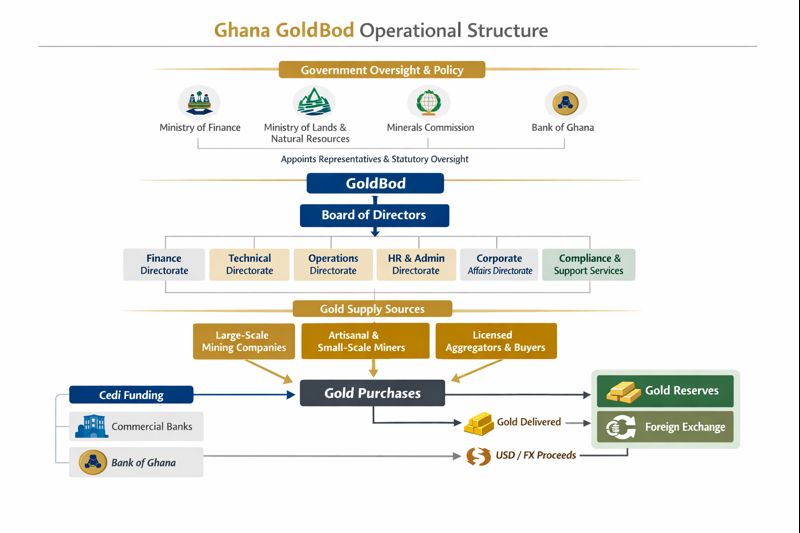

GoldBod (the Ghana Gold Board) was established in 2025 to formalize gold trading from small-scale miners and bolster Ghana’s foreign reserves. The program, essentially an expansion of the Bank of Ghana’s domestic gold purchase initiative, aims to buy gold locally (in cedis), export or sell it for dollars, and use the proceeds to shore up reserves. By design, GoldBod pays local artisanal miners at or even above prevailing world market prices, in order to discourage the rampant gold smuggling that previously deprived Ghana of much export value. While this strategy has yielded some gains – for instance, recorded gold exports from small-scale miners surged from 63.6 metric tons in 2024 to 101 metric tons in 2025 as smuggling was curbed – it also built in a structural cost to the Bank of Ghana (BoG).

When GoldBod buys unrefined doré gold at full price and later sells it internationally, the sale price is lower than the purchase price due to quality discounts, refining costs, and fees. Trading at a loss is practically guaranteed. In October 2025, for example, GoldBod paid miners about $4,054 per ounce but only realized roughly $3,919 per ounce upon export – a shortfall of 3% per ounce. Combine those trading losses with service fees paid to GoldBod, and it becomes clear why the program would generate a net loss for the central bank. Indeed, the IMF’s fifth review of Ghana’s bailout programme disclosed that, by end of September 2025, losses from the artisanal gold purchase component had reached $214 million (about ₵2.4 billion, or 0.2% of GDP) – stemming mostly from trading losses, plus some fees paid to GoldBod’s offtakers. The IMF bluntly warned that “the domestic gold purchase programme poses risks to the financial sustainability of the BoG.” In plainer terms, the central bank has been absorbing large losses to bankroll GoldBod’s operations, which could undermine its balance sheet and, by extension, public finances.

The revelation of the $214 million loss ignited a political and media firestorm in late 2025. It was especially controversial that Ghanaians learned of these losses not from their own government’s reports, but from an IMF document. Critics argue this underscores a troubling lack of transparency: the Gold Board and BoG had not openly acknowledged the mounting losses until external monitors flagged it. With the cat out of the bag, opposition lawmakers seized on the issue, calling for a bipartisan parliamentary probe into GoldBod’s transactions – from procurement processes and pricing formulas to the beneficiaries of service fees. It’s against this backdrop that Sammy Gyamfi stepped forward to defend GoldBod’s track record.

Sammy Gyamfi’s Defense of GoldBod’s Operations

As CEO of GoldBod, Sammy Gyamfi has been the chief spokesperson justifying the program’s outcomes. In statements on December 29, 2025, Gyamfi “challenged claims” that the $214 million figure represents a scandalous failure. Instead, he argues, one must view the losses in context. Gyamfi points out that losses have actually “reduced significantly compared to previous years”. He released preliminary data indicating that under the prior New Patriotic Party (NPP) government’s tenure, the Bank of Ghana’s gold schemes lost a cumulative ₵7 billion in 2023–2024. This includes ₵2.15 billion lost in 2023 and ₵4.84 billion in 2024 across the combined “Gold-for-Oil” and Gold-for-Reserves programs. By contrast, the unaudited loss in 2025 (under the new administration) was about ₵2.3 billion (≈$214 million) for Gold-for-Reserves, with the costly Gold-for-Oil component discontinued. Gyamfi stresses that the opposition NPP has “much higher” blame to bear: “Why demand a probe now,” he asks, when “much higher cumulative losses” occurred under the previous administration without the same outcry?

Gyamfi’s defense is two-pronged. First, he frames GoldBod’s losses as “transactional costs” inherent to an ambitious policy – not evidence of mismanagement or malfeasance. GoldBod is not a profit-seeking company, he notes, but a public tool to acquire reserves. By buying gold at high prices to achieve a public good (currency stability and reserve buildup), some accounting loss was expected. Importantly, Gyamfi claims GoldBod itself hasn’t lost money at an operational level. He maintains that as an institution, GoldBod’s own books are healthy: “GoldBod…has not made any losses,” he stated, revealing that 2025 revenues exceeded ₵960 million against expenditures under ₵120 million, likely yielding a surplus. In other words, the Gold Board collected enough in fees and service charges to cover its direct costs – any net loss sits with the central bank, not with GoldBod’s internal finances. This somewhat technical distinction allows Gyamfi to say GoldBod is financially fine, even if the broader scheme costs the nation money.

Second, Gyamfi leans on macroeconomic results to justify the program’s value. He highlights that 2025 saw a remarkable turnaround in Ghana’s economic indicators, coinciding with GoldBod’s operations. Inflation fell from 23.8% to about 6.3% over the year, and the Ghanaian cedi appreciated over 35% against the US dollar, breaking a decade-long cycle of depreciation. These outcomes, Gyamfi implies, are evidence that the gold strategy is working as intended to stabilize the economy. If the cost of that stability was $214 million in “transactional losses,” he suggests, then so be it – at least those losses “yielded results” in terms of a stronger currency and slowed inflation. Furthermore, supporters note that GoldBod has greatly increased Ghana’s official gold reserves and export earnings by capturing gold that would have been smuggled. In their view, the $214 million should be seen as a “policy cost” – an investment in exchange for macroeconomic stability and formalization of the gold sector.

Politically, Gyamfi has not shied away from an aggressive posture. He accuses the opposition NPP of hypocrisy and vendetta. An NDC-aligned MP, Haruna Mohammed, echoed this, arguing the NPP’s outrage is less about the money and more about punishing Gyamfi for his past criticism of their mismanagement. “He exposed their incompetence, their lies, and their economic mismanagement… in a way they could not counter,” the MP wrote, claiming this is why NPP lawmakers are coming after Gyamfi now. Gyamfi and his defenders repeatedly underscore that losses under GoldBod are far lower now than the “record losses” under the previous government’s gold schemes, and that unlike before, the economy is finally stabilizing. By this narrative, the opposition’s demand for a probe is mere political theater, aimed at discrediting an NDC-led initiative that is actually bearing fruit.

To his credit, Sammy Gyamfi has publicly welcomed calls for a probe – at least in principle. In his December 29 statement, he said GoldBod “is ready to fully cooperate with any investigation” by parliament or other bodies. He promised to provide detailed clarifications on the IMF report and GoldBod’s activities starting the week of January 5, 2026. This indicates an awareness that simply dismissing concerns won’t suffice; hard data and transparency will be demanded in the coming days. The real question is whether Gyamfi’s initial spin and comparative arguments hold up to scrutiny once those details emerge – or whether they have already begun to crumble under the weight of expert analysis and public skepticism.

Questionable Credibility of Gyamfi’s Claims

Despite Sammy Gyamfi’s confident defense, many observers remain unconvinced. The credibility of his arguments has been challenged on several fronts:

Semantic Spin vs. Substance: Gyamfi’s insistence that “GoldBod has made no losses” because the losses sit on BoG’s books strikes some as a semantic dodge. Regardless of which ledger bears the red ink, “a loss recorded by GoldBod or the Bank of Ghana is, by definition, a loss to the State”, as the economic think tank Kandifo Institute bluntly noted. Renaming it a “policy cost” doesn’t erase the economic reality. Ultimately, the Ghanaian public bears that $214 million loss, whether it’s labeled a transaction cost or not. By arguing that GoldBod itself is financially sound, Gyamfi may be factually correct on a narrow point, but he risks appearing disingenuous about the real fiscal impact on the nation.

Selective Use of Data: Gyamfi’s comparative approach – highlighting the NPP-era losses – is a classic “whataboutism” that, while based on real figures, sidesteps the core issue. Yes, BoG’s gold programs lost more money in 2023–24, but that does not automatically exonerate a ₵2.3 billion loss in 2025. The reduction in losses could stem from higher gold prices and program tweaks, not solely superior management. Moreover, critics note that Gyamfi compared audited past losses to unaudited current figures, which is premature. The opposition warns 2025’s losses might reach $300 million by year-end, once fully accounted. Gyamfi’s credibility suffers if he appears more eager to score political points against his predecessors than to candidly assess the effectiveness of GoldBod’s model going forward.

Attributing Macroeconomic Wins: Touting the cedi’s appreciation and inflation’s decline as proof of GoldBod’s success is also problematic. Independent analysts caution that 2025’s macro stabilization had multiple fathers, not just GoldBod. The Kandifo Institute points out that an IMF-supported stabilization program was underway, including debt restructuring, fiscal tightening, high global gold prices, and tight monetary policy, all of which contributed to improving indicators. It is “serious attribution bias” to credit GoldBod alone for the cedi’s rise. In fact, some of GoldBod’s apparent benefits (like lower cedi-denominated debt servicing costs and cheaper imports) are simply a byproduct of the stronger exchange rate, “not real resource gains”, as Kandifo notes. Gyamfi’s narrative may therefore overstate GoldBod’s singular impact, undermining his argument that the $214 million was a small price to pay for stability.

“Loss or No Loss” Confusion: By downplaying the loss as “not a loss,” Gyamfi waded into a technical debate that even experts find nuanced. A Business & Financial Times analysis mused that the GoldBod debate has been “passionate, sentimental, and technical all in one,” with some contending it’s a loss and others arguing it’s an acceptable cost. But as that analysis explains, in economic policy the line between cost and loss hinges on whether the policy’s benefits justify the expense. So far, Gyamfi has highlighted benefits without fully addressing whether the same outcomes could have been achieved more efficiently. By seeming to dismiss the IMF’s characterization of a trading loss (which was based on data given by his own institution to the Fund), Gyamfi might appear “in over his head” – not fully grasping the financial seriousness or simply ignoring inconvenient facts. The IMF’s position was not a speculative attack; it came from Ghana’s own reports to the Fund and was labeled “emphatic” and grounded in treaty obligations that ensure rigorous monitoring. Challenging the IMF’s terminology, as GoldBod initially did, risked Gyamfi’s credibility. As policy expert Bright Simons quipped, if one chooses to distrust the IMF on this negative finding, “then why should we trust anything else they say about the economy, including the good stuff?” – a pointed reminder that one cannot cherry-pick IMF reports for convenient truths.

Professionalism and Partisanship: Perhaps the most biting critique of Gyamfi’s performance is that he has handled this as a partisan communicator rather than a technocratic CEO. Even some who don’t contest his numbers took issue with his tone. Tweneboa Kodua Fokuo, an opposition (NPP) Member of Parliament, called Gyamfi’s response “unfortunate” and unbefitting of a CEO. “If you are a CEO and [a] significant loss like this [occurs] through your activities… I am surprised to see you on social media [saying] I have a loss but NPP also made losses,” Fokuo remarked, suggesting Gyamfi sounded more like a party propagandist than a responsible public manager. That critique resonates with non-partisan observers who expect a level of humility and accountability from officials in charge of public funds. By immediately shifting blame to political opponents, Gyamfi may have eroded trust among Ghanaians who simply want transparency and solutions. It also raises the question: is Gyamfi out of his depth, relying on spin because he lacks a better explanation? The optics of a high-ranking NDC figure seemingly making excuses about missing millions feeds a narrative that he may not fully comprehend the complexities of the program he’s administering.

In sum, while Sammy Gyamfi has marshaled data and rhetoric in GoldBod’s defense, the effectiveness of his arguments is debatable. He has highlighted true facts (previous losses, macro gains) but often in a way that dodges the crux of the issue – that Ghana’s central bank has bled substantial funds in this gold venture, and the public was kept in the dark until an outside audit (the IMF review) exposed it. His credibility will ultimately hinge on whether he can move beyond political talking points and engage in a frank, detailed accounting of GoldBod’s operations.

Transparency and Accountability Concerns

One of the most troubling aspects of the GoldBod saga – and Gyamfi’s stewardship – is the opaque manner in which GoldBod has operated. From its inception, GoldBod’s activities have been shrouded in limited disclosure, leading to questions about accountability. Several transparency issues have emerged:

Delayed Disclosure of Losses: As noted, it took an IMF report to reveal the extent of GoldBod/BoG’s trading losses to the Ghanaian public. Prior to that, no regular public reports had flagged a $214 million drain in 2025. GoldBod’s CEO Franklin Cudjoe (the IMANI Africa president) lamented, “my worry though is that it had to take the IMF to receive this information and then publish [it] for us to knock our heads… Not good!”, expressing dismay that Ghanaians learned of the loss second-hand. Gyamfi and GoldBod did not proactively share this critical information, which undermines claims of transparency.

Refusal to Release Data: Bright Simons of IMANI revealed a pattern of GoldBod stonewalling information requests. He noted months of back-and-forth where GoldBod’s management “keep refusing to release information on [their] trades”, only for the IMF to finally “confirm what we have been saying for months.” This suggests a deliberate lack of openness. If GoldBod had nothing to hide, why would it withhold trading details from policy analysts and, by extension, the public? Such opacity fuels suspicions: whether of inefficiency, poor oversight, or even corrupt dealings (though no concrete evidence of corruption has been presented as yet, the environment of secrecy is fertile ground for doubt).

Books Not Reflecting Losses: GoldBod’s accounting stance appears to be that these are BoG’s losses, not GoldBod’s. Franklin Cudjoe observed that GoldBod doesn’t acknowledge the losses on its books because it sees itself as an intermediary between BoG and gold aggregators. While that might be technically how the accounting is structured, it means GoldBod can claim a clean balance sheet while the central bank quietly absorbs all the damage. This separation lacks transparency and accountability, effectively passing the buck. Cudjoe insists that we need to know “how [the $214m loss] occurred, the period it occurred and where… as in with which buyers of our gold and the quantum of loss per buyer”. In other words, a granular breakdown of those losses is needed – information GoldBod should have but had not disclosed publicly. Without it, stakeholders can’t tell if the losses were evenly spread, or if certain transactions or partners caused outsized costs (raising red flags).

Questions on Procurement and Pricing: The Minority in Parliament’s call for a probe is specifically to scrutinize GoldBod’s procurement practices, fee arrangements, and pricing formulas. This implies concerns that the rules governing GoldBod’s deals may not be robust or transparent. For example, who are GoldBod’s “offtakers” and aggregators, and on what terms are they engaged? It emerged that a company called Bawa Rock Ltd was designated as the apex aggregator for small-scale gold, enjoying interest-free financing from BoG that private competitors did not get. This kind of preferential arrangement, if poorly disclosed, can breed allegations of cronyism. Is Bawa Rock delivering value commensurate with that support, or did it have political connections? Only full disclosure of contracts and outcomes can dispel such suspicions. Furthermore, pricing strategy – paying above spot price, as GoldBod sometimes did – needs justification and oversight. Was there a clear policy on how much above market to pay, or was it ad hoc? Transparency would allow experts to verify if the pricing was optimized or if the state overpaid unnecessarily in some cases.

Lack of Audited Financials: As of the end of 2025, GoldBod had been operating for around a year but had not published audited financial statements. Gyamfi himself repeatedly refers to “unaudited” figures for 2025. While it’s understandable that final audits lag the fiscal year, the absence of any interim financial reporting means Ghanaians have little official data on GoldBod’s revenues, expenses, and financial position besides what Gyamfi selectively shared. This vacuum of official reporting is precisely what allowed wildly different narratives to flourish – from “GoldBod is profitable” to “GoldBod is a black hole”. Releasing audited statements and detailed reports to Parliament could greatly enhance credibility. Without them, Gyamfi is effectively asking the public to “trust me, I have the numbers” – a big ask given the political polarization.

Encouragingly, both government-aligned voices and independent analysts agree on one point: transparency must improve. Franklin Cudjoe, even as he commended the concept of GoldBod, urged the BoG to explain the losses clearly and minimize future occurrences. Bright Simons hammered that information given to the IMF “should have been shared… long ago” with domestic stakeholders. And Sammy Gyamfi, feeling the pressure, has now committed to providing clarifications and cooperating with investigations. The coming probes and reports will test whether GoldBod’s leadership truly embraces transparency or continues to be defensive. For Gyamfi, it’s an opportunity to shed the image of opacity by opening the books – but any hesitation or half-measures will likely be seized upon as proof that he was in over his head and trying to hide the mess.

Political Fallout for Opposition and Ruling Parties

The GoldBod controversy has swiftly been weaponized in Ghana’s charged political arena, with both the ruling party (NDC) and opposition (NPP) seeing it as fodder for their narratives. The issue illustrates how economic policies, even technical ones, are never far from politics in Ghana:

Ruling Party (NDC) Dynamics: Sammy Gyamfi is a prominent member of the National Democratic Congress, having built a reputation as a sharp-tongued communications director in opposition. Now in government (following the NDC’s return to power in 2025), Gyamfi’s handling of GoldBod reflects on the NDC’s competence. The party’s supporters and officials have closed ranks around him so far. They emphasize that GoldBod is yielding positive outcomes and cleaning up a mess inherited from the NPP. The NDC is touting the drop in inflation and currency stabilization as vindication of its economic management, implicitly crediting GoldBod and by extension Gyamfi’s leadership. However, this could become a double-edged sword. If investigations reveal any mismanagement, or if losses continue to mount beyond projections, the NDC government will own those failures. There is also the optics issue: appointing a partisan firebrand to head a sensitive financial program invites criticism that meritocracy was sidelined for loyalty. If Gyamfi falters or if his explanations don’t hold water, it won’t just be his personal reputation at stake – the credibility of President Mahama’s administration could suffer. The NDC must balance defending GoldBod as a government policy with ensuring accountability. Any perception of a cover-up or whitewash in the promised probe would undermine the government’s anti-corruption stance. Thus far, President Mahama’s team seems willing to defend GoldBod to the hilt, betting that it will be seen as a tough but necessary intervention that the NPP lacked the vision or courage to implement. The political calculus is that Ghanaians will appreciate the immediate economic relief (stable prices, stable currency) enough to overlook an abstract loss figure. But that calculus could change if the conversation shifts to where that $214 million might have gone – potentially lining private pockets or simply wasted due to poor design.

Opposition (NPP) Strategy: For the New Patriotic Party, now in opposition, GoldBod’s losses are a convenient rallying point to attack the NDC government’s competence. NPP lawmakers have aggressively pushed the narrative that GoldBod is a boondoggle – opaque, poorly managed, and possibly a conduit for corruption or favoritism (they often hint at the need to investigate who benefited from the gold trades and fees). The Minority in Parliament’s formal call for a bipartisan inquiry signals that the NPP wants to keep this issue alive and in the headlines. They sense vulnerability in Sammy Gyamfi, given his lack of prior experience in economics and finance, and they are eager to depict him as out of his depth, mishandling public funds. However, the NPP faces its own credibility issues: GoldBod’s precursor programs were initiated under their watch in 2021–2022, and as Gyamfi never ceases to point out, those years saw even greater losses with arguably less to show for it. NPP communicators have been somewhat selective, sometimes framing the issue as “Mahama’s government has lost $214m on a risky gold gamble,” without acknowledging that the gamble began under Akufo-Addo’s government. Even so, the NPP’s angle is that the NDC scaled up the program (via GoldBod) in 2025 and should have known better how to mitigate losses. They claim the current structure is “deeply flawed and opaque,” warning that Ghana could “lose up to $300 million in 2025” if it continues unabated. Essentially, the opposition seeks to brand GoldBod as another example of NDC mismanagement – akin to past scandals – to gain leverage in public opinion and future elections.

Polarized Public Perception: Public reaction to the GoldBod issue often mirrors party lines, but not entirely. Many ordinary Ghanaians are primarily concerned with tangible economic conditions. By late 2025, they saw inflation easing and the currency recovering value – rare good news after years of hardship. That fosters some public tolerance for GoldBod’s costs, especially among NDC sympathizers who view it as “taking one step back to take two steps forward.” On the other hand, hearing that the central bank lost $214 million is infuriating to many, especially in a country that just went through a painful debt restructuring. There’s a sentiment of “here we go again with political elites playing fast and loose with public funds.” The fact that Sammy Gyamfi was a vociferous critic of financial scandals in the previous government is not lost on the public; some now see a role reversal verging on irony. Social media commentary and radio phone-in shows have been buzzing with questions: If GoldBod is so above board, why weren’t we told about the losses sooner? If it’s a great policy, why is there such defensiveness and blame-shifting from its CEO? In this climate, expert voices have significantly shaped perception.

Franklin Cudjoe (IMANI) has somewhat balanced views that resonate with moderates. He acknowledges the innovative intent of GoldBod and commends the government for learning from past mistakes, but he insists on transparency about the losses and how to minimize them. His stance suggests one can support the policy goals while demanding accountability – a nuanced view that likely reflects a segment of the public who favor long-term solutions but worry about execution.

Bright Simons (IMANI VP) has taken a harder line, clearly skeptical of GoldBod’s management. His vocal critiques – calling out “accountability deficits and opacity” – energize those who fear GoldBod could be a cover for something untoward. Simons even highlighted fairness issues, like the unlevel playing field for private gold aggregators versus a state-backed one. Such points raise broader concerns about whether GoldBod’s model might be crowding out private enterprise or breeding inefficiency under the guise of state control. For Ghanaians suspicious of big government projects, Simons’ warnings strike a chord.

Outside think tanks, even industry stakeholders have chimed in. The Chamber of Licensed Gold Buyers reportedly clarified that the losses stem in part from the price GoldBod paid miners (which included regulated margins), seemingly to argue there’s no theft – just the cost of doing business at fair prices. This suggests those within the gold trading industry want to ensure the narrative doesn’t turn into finger-pointing at them.

Ultimately, the political implications of the GoldBod episode are still unfolding. If Sammy Gyamfi manages to convincingly clear the air – showing that the losses were controlled, yielded net benefits, and that no funds went missing – the ruling NDC may turn this into a story of prudent governance (i.e. “we fixed a broken system and saved Ghana money compared to what the NPP was doing”). In that scenario, Gyamfi could even emerge as a bold innovator who endured criticism to achieve results. However, if the forthcoming probe or data dump reveals deeper problems (say, procurement irregularities, larger losses than admitted, or unsustainable practices), the opposition will have a field day and Gyamfi’s political future will be in jeopardy. It could reinforce an age-old narrative in Ghanaian politics: that well-meaning schemes end up as vehicles for waste or graft when entrusted to partisan operators. The title of this article – “Sammy Gyamfi is in Over His Head” – would then echo not just as a critique of one man’s performance, but as a cautionary tale about political overreach into complex economic policy.

Public and Expert Opinions: Is Gyamfi Sinking or Swimming?

Public perception of Sammy Gyamfi’s handling of GoldBod is a mix of applause, criticism, and confusion. Expert opinions have been equally divided, and together they shape whether Gyamfi is seen as rising to the challenge or floundering. Here’s a snapshot of the spectrum:

Supporters’ View: Among ruling party loyalists and some policy commentators, there is a narrative that Gyamfi is being unfairly maligned for a necessary policy. They argue that a $214 million “loss” is a calculated investment to achieve bigger goals. Businessman Senyo Hosi articulated this view, framing the GoldBod losses as an “acceptable policy cost” given the macroeconomic gains. Hosi and others credit GoldBod (and by extension Gyamfi) with stabilizing the cedi, building reserves, and taming inflation, outcomes that benefit all Ghanaians. They also highlight the achievement in curbing gold smuggling – a perennial problem – through savvy pricing strategies that Gyamfi oversaw. To this camp, Gyamfi is a bold problem-solver, willing to break an old paradigm (of cheaply selling Ghana’s gold abroad) and think outside the box. They view the opposition’s attacks as politically motivated, aimed at tarnishing an NDC success. Indeed, supporters like MP Haruna Mohammed praise Gyamfi for “exposing [the NPP’s] incompetence” in the past and see the current backlash as revenge, not genuine concern. On social media, NDC-inclined voices often echo Gyamfi’s stats about the NPP’s ₵7 billion losses, arguing that at least Gyamfi’s team reduced the damage and turned the trajectory positive. The phrase “transaction cost” is used to imply that nothing nefarious happened – it was a known expense for a strategic outcome. In short, this side believes Sammy Gyamfi is on the right track, albeit learning on the job, and that history will vindicate the GoldBod experiment if given time.

Critics’ View: Detractors, however, see Gyamfi as overmatched by the complexity of managing Ghana’s gold resources. They point to what they call amateurish handling – from the defensive communications to the lack of full disclosure. Policy experts at the Kandifo Institute challenge the rosy spin, emphasizing that financial losses can’t be wished away by good intentions. They worry that GoldBod under Gyamfi has essentially turned the BoG into a vehicle for subsidizing miners and traders, creating “market distortions on the central bank’s balance sheet” rather than fixing systemic issues. This view holds that Gyamfi might not grasp the long-term risks: if gold prices fall or currency pressures return, Ghana could be stuck with a mounting bill and a weakened central bank. In other words, the strategy is only as good as the conditions that favored it in 2025. Critics also note Gyamfi’s lack of relevant background – prior to this role, he was a lawyer and political communicator, not an economist or trader. This fuels the perception that he may be in over his head technically, relying on advisors or trial-and-error. Instances like the public rebuttal of the IMF’s wording (only to semi-concede later) suggest to skeptics that Gyamfi is “winging it”. Publicly, opposition figures have not minced words: some have called for Gyamfi to resign or be fired if an inquiry finds negligence. Among everyday citizens critical of the government, one finds sentiments like “they put a propaganda guy in charge of our gold, what did you expect?” – a harsh assessment of Gyamfi’s suitability.

Neutral/Analytical View: There is also a segment of observers taking a wait-and-see stance. These individuals acknowledge the potential benefits of GoldBod but insist on proper oversight and mid-course corrections. For example, Franklin Cudjoe’s stance is neither full-throated praise nor outright condemnation. He applauds the innovative approach and learning from past mistakes (implying Gyamfi’s team adjusted some flaws from the NPP era), yet he simultaneously demands that BoG and GoldBod open up their records on the losses. Cudjoe’s nuanced position likely reflects a portion of the public that is pragmatic – they don’t care which party implements a policy as long as it works and is accountable. For them, the upcoming parliamentary probe is crucial. A clean bill of health (or a transparent admission of controllable losses) could validate GoldBod, whereas any whiff of scandal will confirm their worst fears about political meddling in economic policy. Similarly, some financial journalists and independent economists have treated GoldBod as an experiment: they dissect its mechanics (like JoyNews did in a detailed analysis of how the losses occur) and suggest tweaks rather than scrapping it outright. This middle-ground perspective sees Sammy Gyamfi as neither savior nor villain, but as a political appointee navigating an inherently tricky policy. They worry about moral hazard – if political figures believe central bank losses don’t matter, it sets a bad precedent – but they also see the value in capturing Ghana’s gold for national benefit.

In the court of public opinion, Sammy Gyamfi’s fate is still being decided. He has ardent defenders and harsh critics, but the vast majority will judge him on results and integrity. If the promised disclosures in early 2026 come forth and show that everything was above board – that the $214 million “loss” indeed bought Ghana substantial gains and was not padded by any graft or undue profiteering – then Gyamfi could restore trust and maybe even emerge stronger. On the other hand, if more skeletons tumble out (for instance, if the losses turn out to be higher, or if certain transactions benefited politically connected parties disproportionately), public perception will sour dramatically. Already, Ghana’s history with public financial scandals (from bond deals to procurement overspending) casts a long shadow – people have learned to be skeptical.

Right now, many Ghanaians are scratching their heads at the mixed messages: IMF says there’s a big loss, GoldBod says “it’s not a loss, we’re actually doing great”, the opposition cries “scandal”, the government counters “previous scandal was worse”. This cacophony doesn’t inspire confidence. The onus is on Sammy Gyamfi to cut through the noise with hard facts and transparency. Anything less, and the label “in over his head” will stick – not just as an insult, but as a tangible reality evidenced by a faltering GoldBod and a disillusioned public.

Conclusion

Sammy Gyamfi’s plunge into the deep waters of economic policy has proven both bold and precarious. Charged with overseeing Ghana’s novel gold-for-reserves program, he has had to transition from partisan crusader to institutional leader – a shift that has tested his capabilities. On one hand, GoldBod’s first year coincided with notable economic improvements and a clampdown on gold smuggling, suggesting that the policy is not without merit. On the other hand, the $214 million loss reported by the IMF looms large, raising fundamental questions about sustainability, transparency, and accountability. Gyamfi’s initial response to this challenge was combative and politicized: he pointed fingers at his predecessors and downplayed the losses as mere costs of doing business. Such defensiveness is understandable – after all, his reputation and the government’s credibility are at stake – but it also reinforced the perception that he may be out of his depth.

The coming months will be decisive. If Gyamfi truly isn’t “in over his head,” he will need to demonstrate it by embracing full transparency, heeding the calls for rigorous audits, and showing a willingness to adjust GoldBod’s model to reduce future losses. He will have to engage not just in public relations, but in public accountability – a far more uncomfortable arena. In Ghana’s vibrant democracy, where a ferocious opposition and a vocal civil society are always ready to pounce, anything less will not suffice. For now, Sammy Gyamfi is balancing on a fine line: between policy success and failure, between political point-scoring and genuine accountability. How he navigates the intense scrutiny ahead will determine whether he sinks under the weight of GoldBod’s controversy or swims to shore with his credibility intact. At this juncture, as the evidence stands, many observers are convinced that Gyamfi has ventured into waters deeper than he anticipated – and perhaps deeper than he can handle. The title of CEO brought him prestige and influence, but it also brought a harsh spotlight. To survive it, Gyamfi must remember that in matters of public trust, substance counts far more than spin. The nation watches and waits to see if he can rise to the occasion, or if indeed, Sammy Gyamfi is in over his head.

Sources: The analysis above draws on a range of Ghanaian media reports, expert commentary, and financial reviews. Key references include JoyNews’ breakdown of GoldBod’s losses, statements from Sammy Gyamfi himself as reported by Citi News, commentary from IMANI Africa’s Franklin Cudjoe and Bright Simons highlighting transparency issues, as well as responses from political figures on both sides of the aisle. Financial insights from the IMF’s 5th Review and critiques by the Kandifo Institute have also been incorporated to provide a balanced perspective.

Leave a comment